While the second quarter was bad from a macro economic perspective, technology once again appears to be impervious to crises. The NASDAQ is at an all-time high, mostly driven by big tech stocks. Taking a step back, the market crash in March now just looks like a minor dip. What about European venture capital? After a period of shock in March/April, risk appetite is coming back.

Investment is down 21% vs. 2019

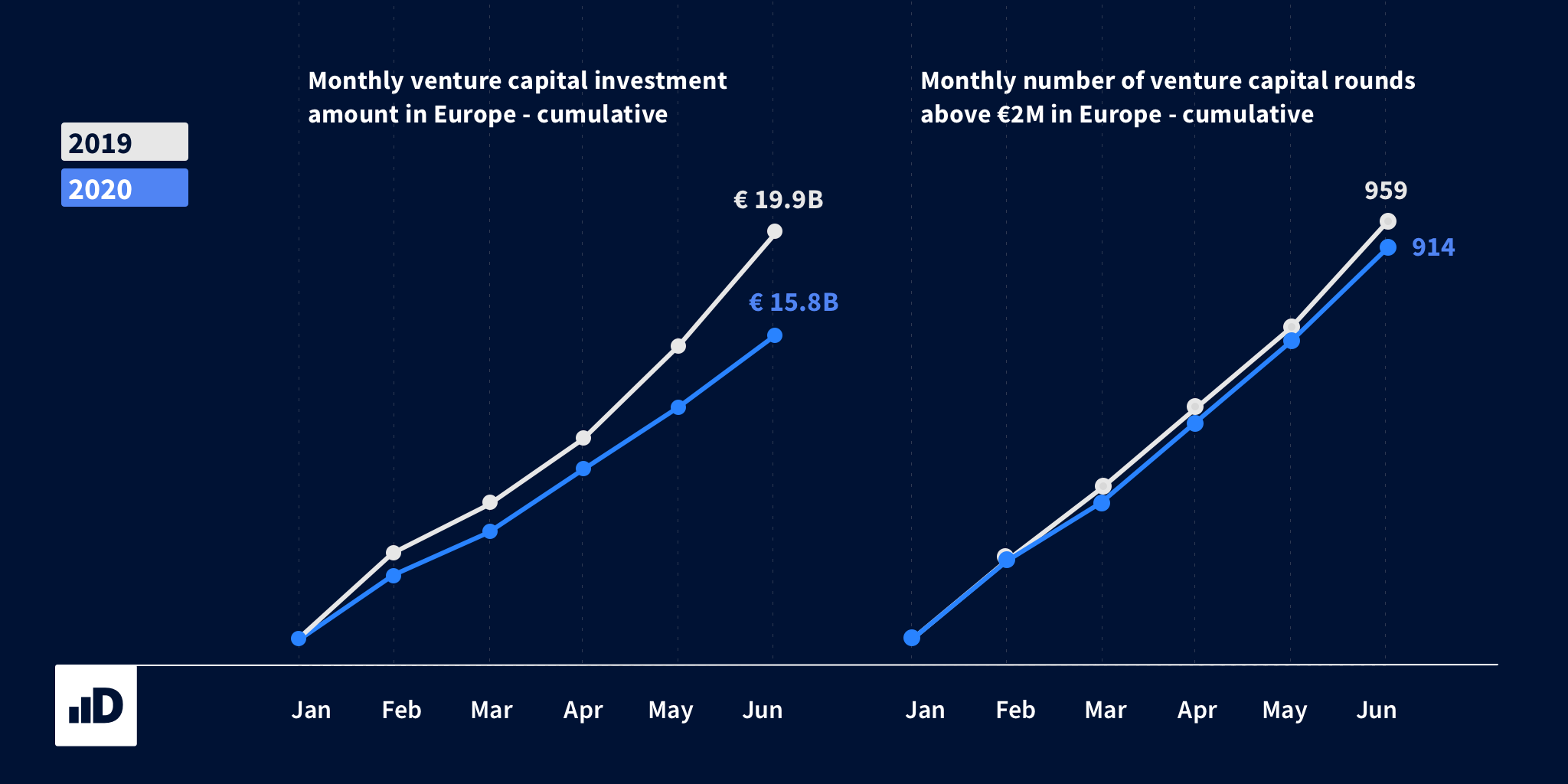

For the first 6 months, European startups raised €15.8 billion, down 21% versus the same period last year. Surprisingly however, the number of rounds is almost the same as last year. Only rounds above €2 million are measured here because they’re less affected by reporting lag.

Does this mean that investment tickets were lower? What is the underlying data telling us? The data platform provides the answers.

Q2 2020 is up 5% compared to Q1

Venture capital investment in Europe reached €8.1 billion in Q2 2020. This is up 5% compared to the previous quarter and down 27% from Q2 2019. Check out the below link to view all underlying deals.

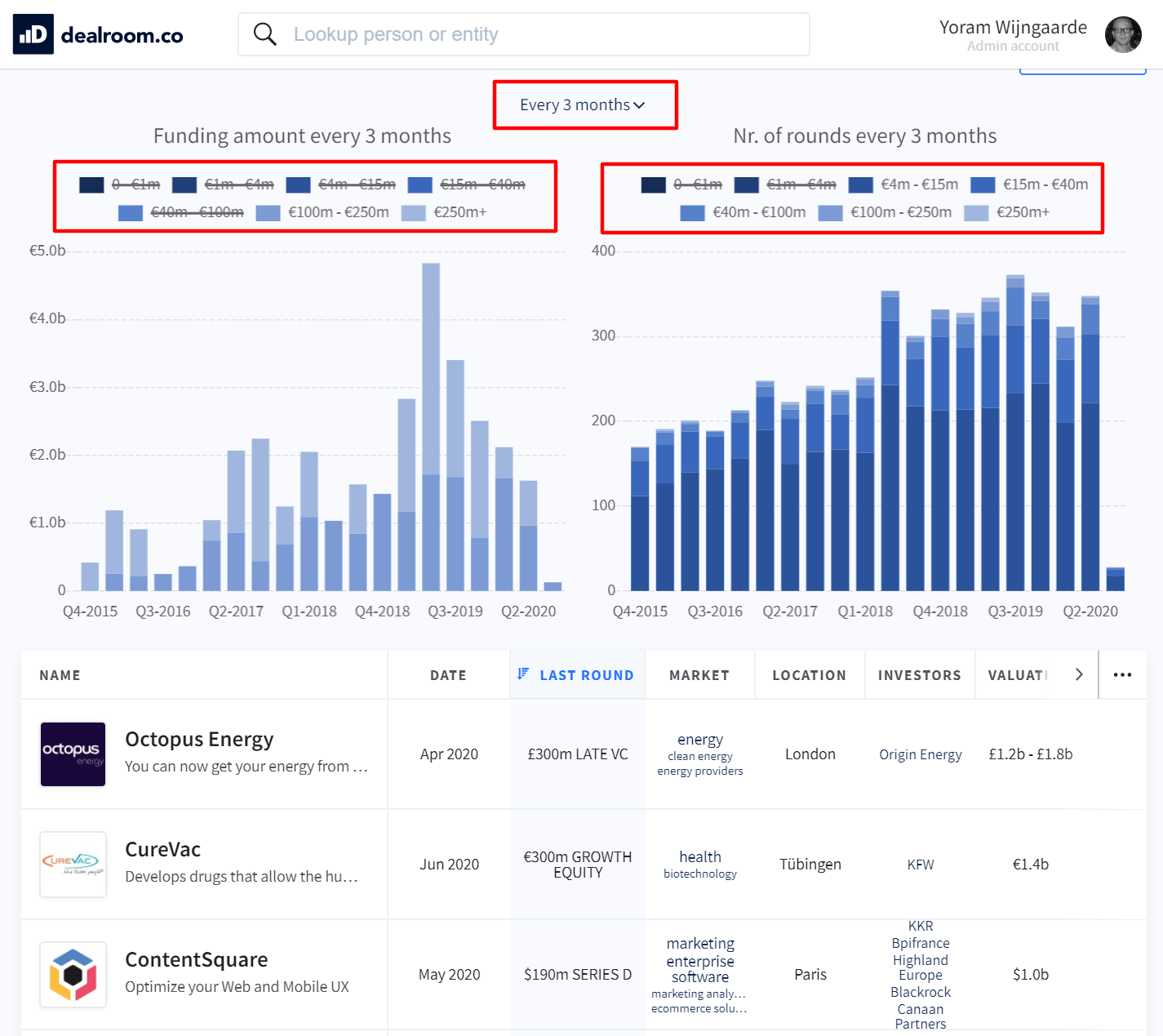

Far fewer mega+ rounds

The charts also indicate a drop of “mega rounds” (€100M) and “mega rounds plus” (€250M). You can visualize this even more clearly by hiding other rounds from the chart (the legend itself is clickable). The same way, you can visualize how the number of rounds in the “mid range” (€4–40M) are still growing. Tip: you can also switch to monthly data, which shows that the main dip happened in March.

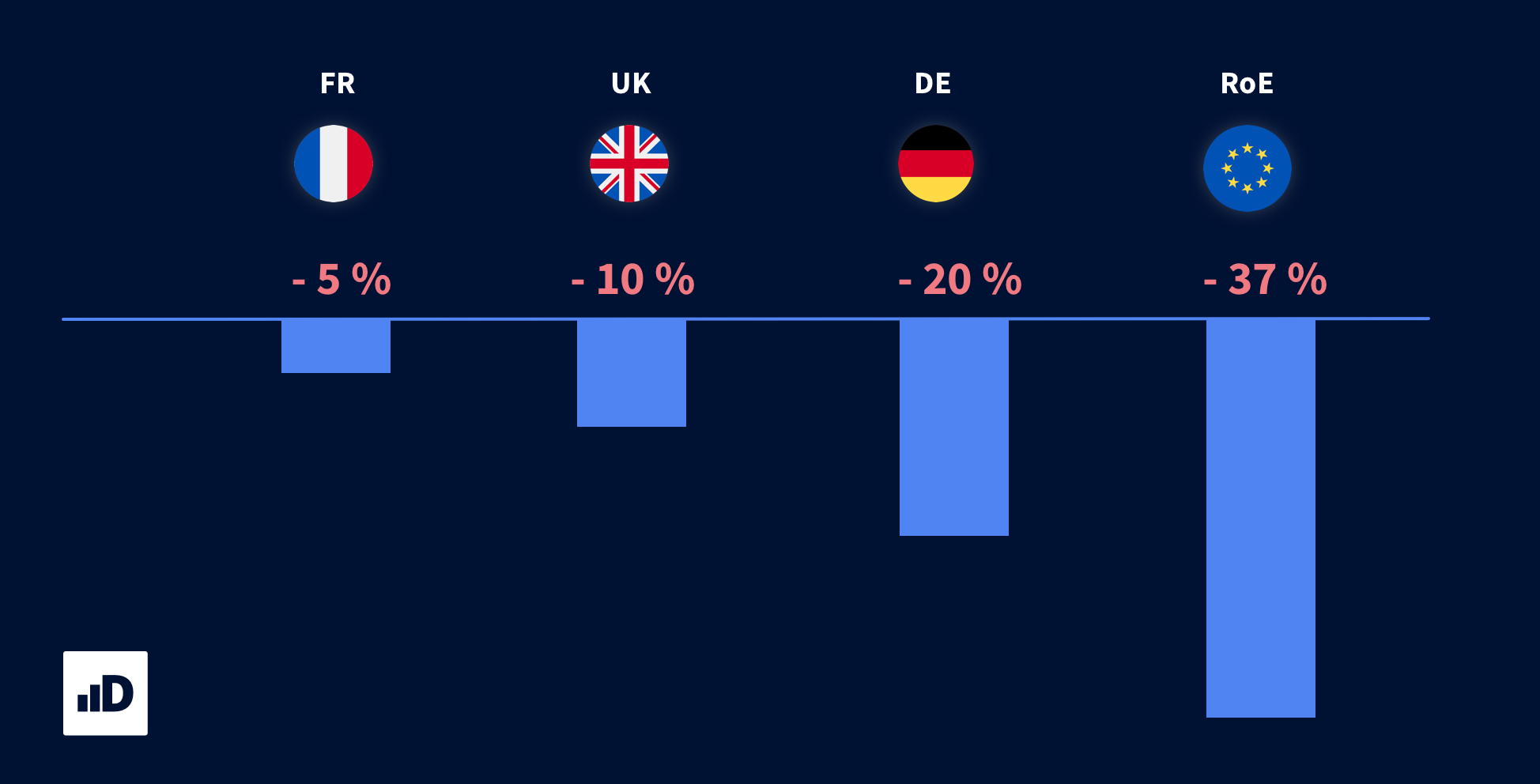

UK, France, and Germany holding up. Rest of Europe more impacted

The UK and France appear to have been barely impacted by the pandemic so far. Based on headline investment numbers for H1 2020, the UK and France are down only 10% and 5% respectively. Germany is down 20%, but that decline is driven by a handful of mega rounds plus last year. In the rest of Europe however, investment is down 37%.

The UK, France and Germany each have the largest pool of established and high-quality startups that are more likely to receive follow-on funding from their investors, making these markets more resilient during crises. France is the least affected, likely related to the government being most decisive in providing rapid crisis support. The fact that French investment is substantially domestic, likely also played a role.

Investment is up again in Q2 in most European countries

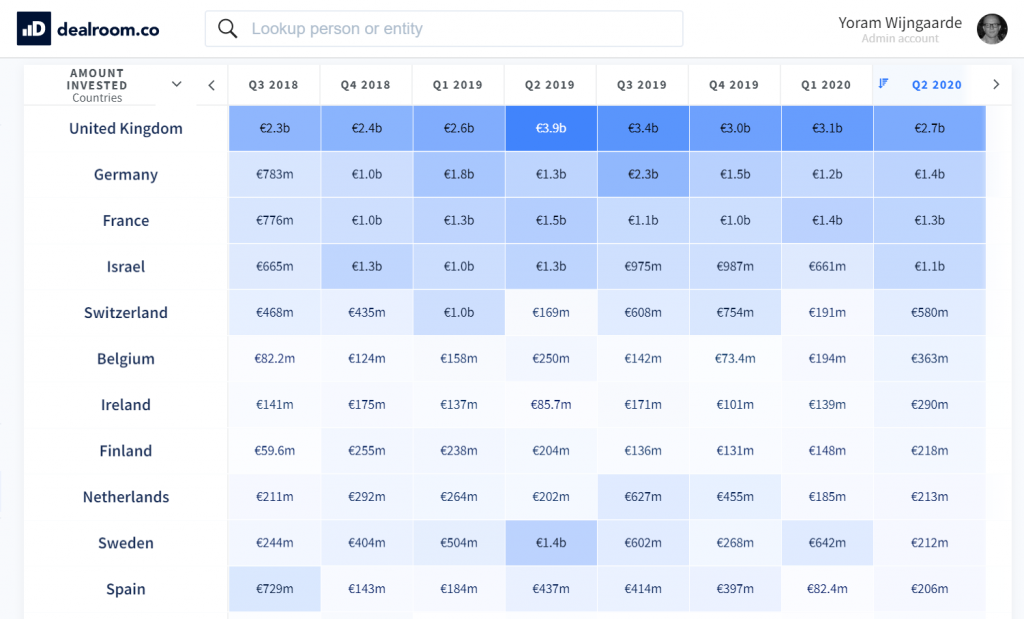

What are the dynamics in the rest of Europe? The data platform shows us that hubs like Spain, Netherlands and Switzerland experienced sharp drops in Q1 investment activity. In Q2, investment activity has recovered across most countries.

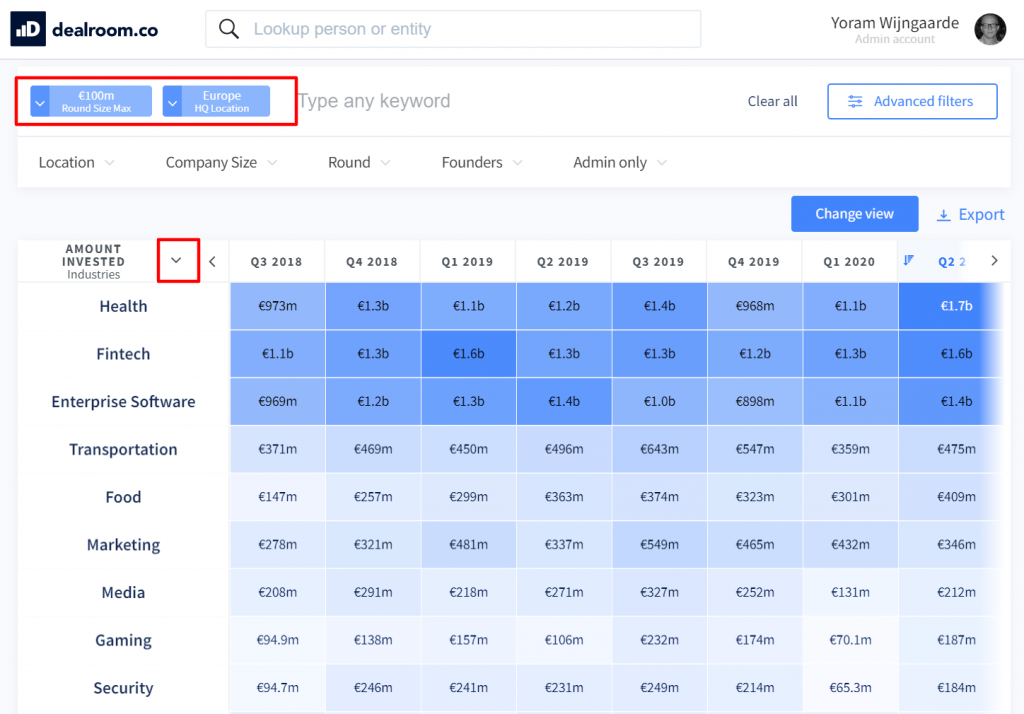

Health tech, fintech, SaaS, mobility receive bulk of investment

Below is the same investment heatmap, but switching the output to industries instead of countries. You can do this by using the dropdown menu marked red. In the below heatmap, mega rounds have been excluded to get a better view of underlying trends. But you can change the filters as you want them, directly on the platform.

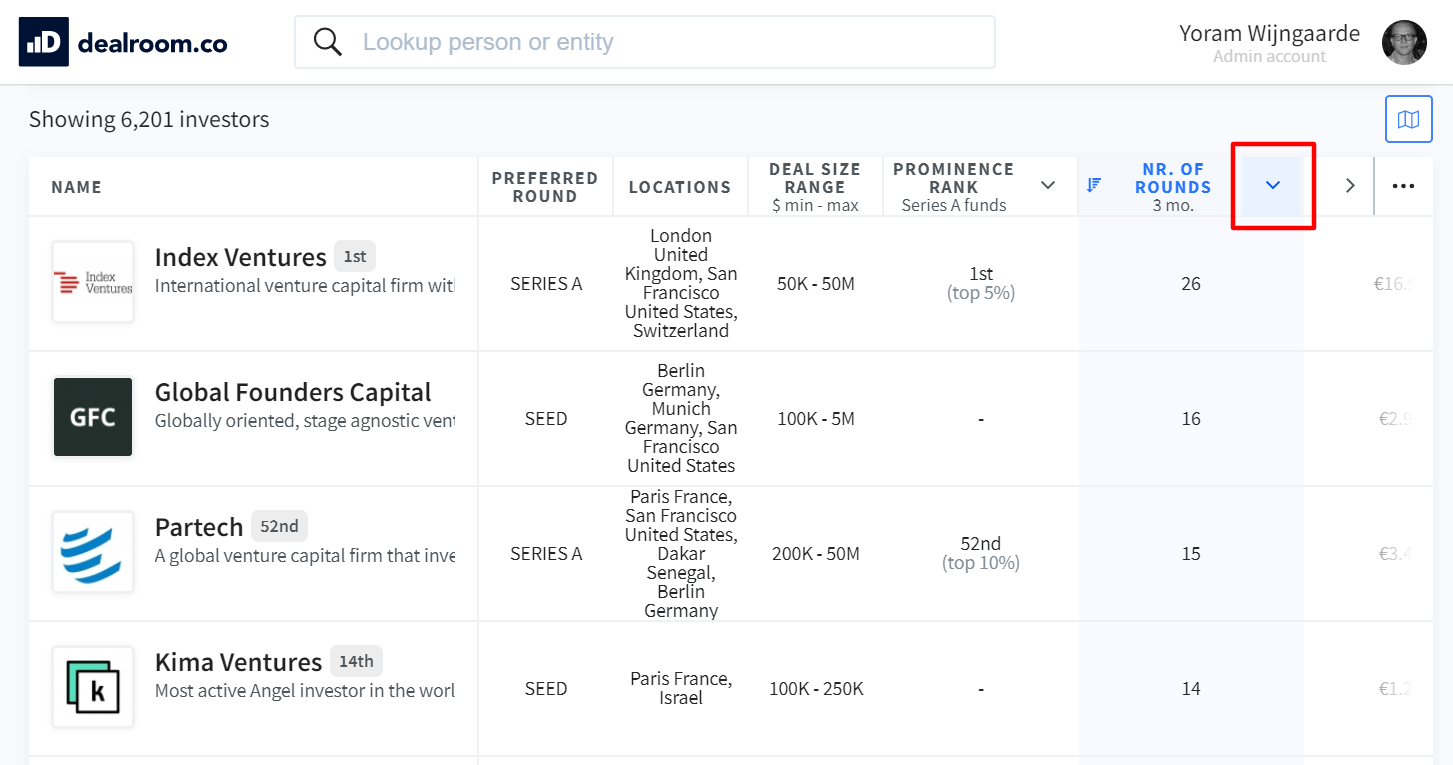

The most active VCs in Q2 2020

In late May, we published a blogpost on the top 20 Europe’s most active VCs in 2020. Below is the full list of most active VCs based on Q2 2020 data. Tip: use the filters so see which investors are most active in your market.

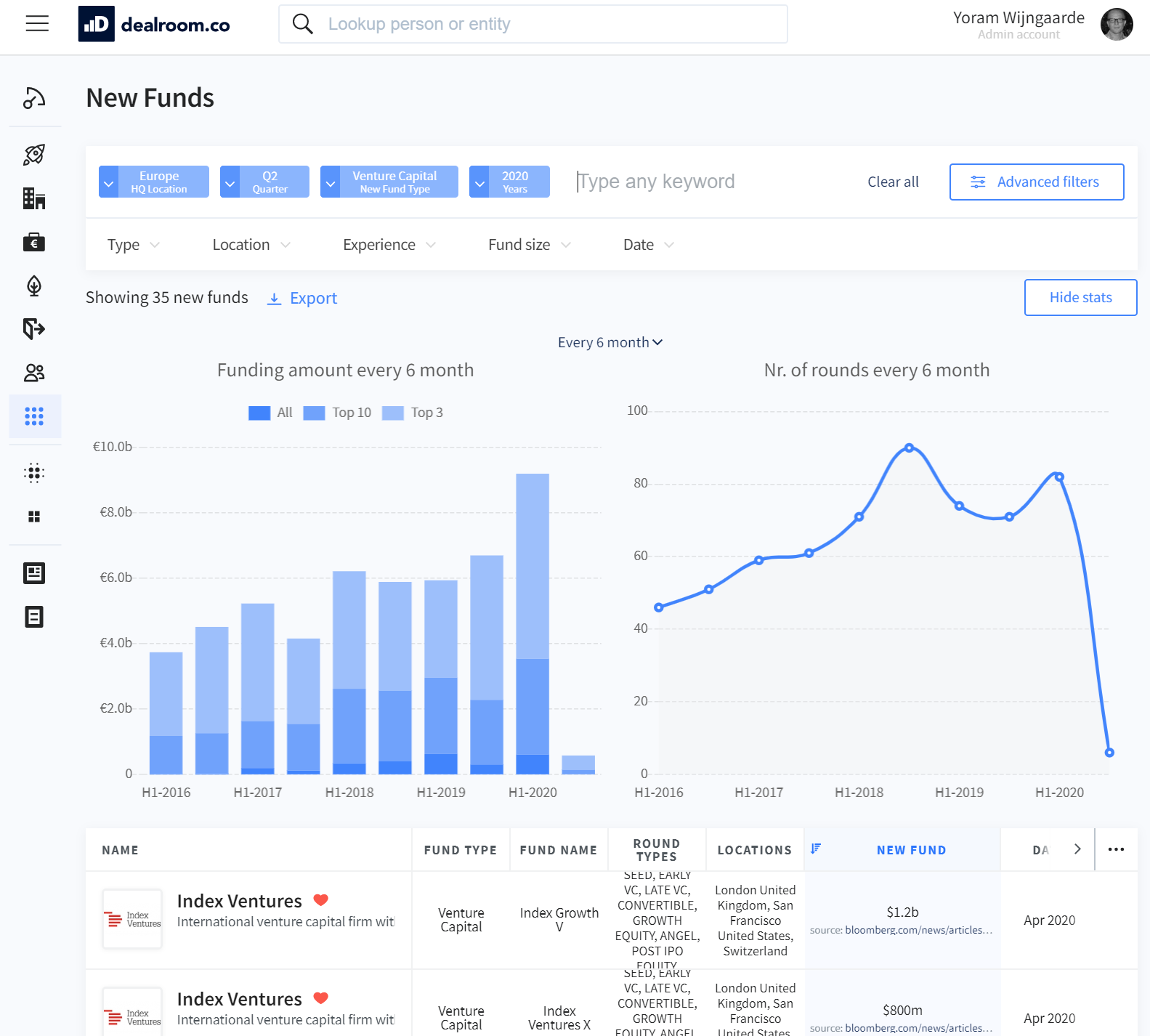

New VC funds raised reached an all-time record

In the first half of 2020, European VCs not only continued to raise significant funds. They raised more than ever before. The previous record was Q2 2019. This means there’s more dry powder than ever ready to be deployed into European startups in the rest of 2020 and beyond. Check out the underlying data by clicking on the below image.