Naspers will be investing €387 million (about $420 million) for a minority stake in Delivery Hero, the global food delivery marketplace, at a valuation in line with Delivery Hero’s previous valuation, said Naspers’ statement. In a Tweet, Naspers calls it a “pre-IPO round”. Assuming a $3.1 billion pre-money valuation, Naspers will own around 12% while Rocket Internet’s ownership will go from 38% to 33%. Naspers will also take one seat on Delivery Hero‘s Supervisory Board.

The valuation represents a multiple of about 10x 2016 net revenues, which is similar to Just Eat (10x) and slightly below Takeaway.com (11x). For 2017E, the multiple is 7.5x net revenues, a slight discount versus Just Eat (8x) and Takeaway.com (8.5x). Note that Naspers’ investment likely comes with downside protection e.g. in the from of a liquidation preference, distorting the comparison.

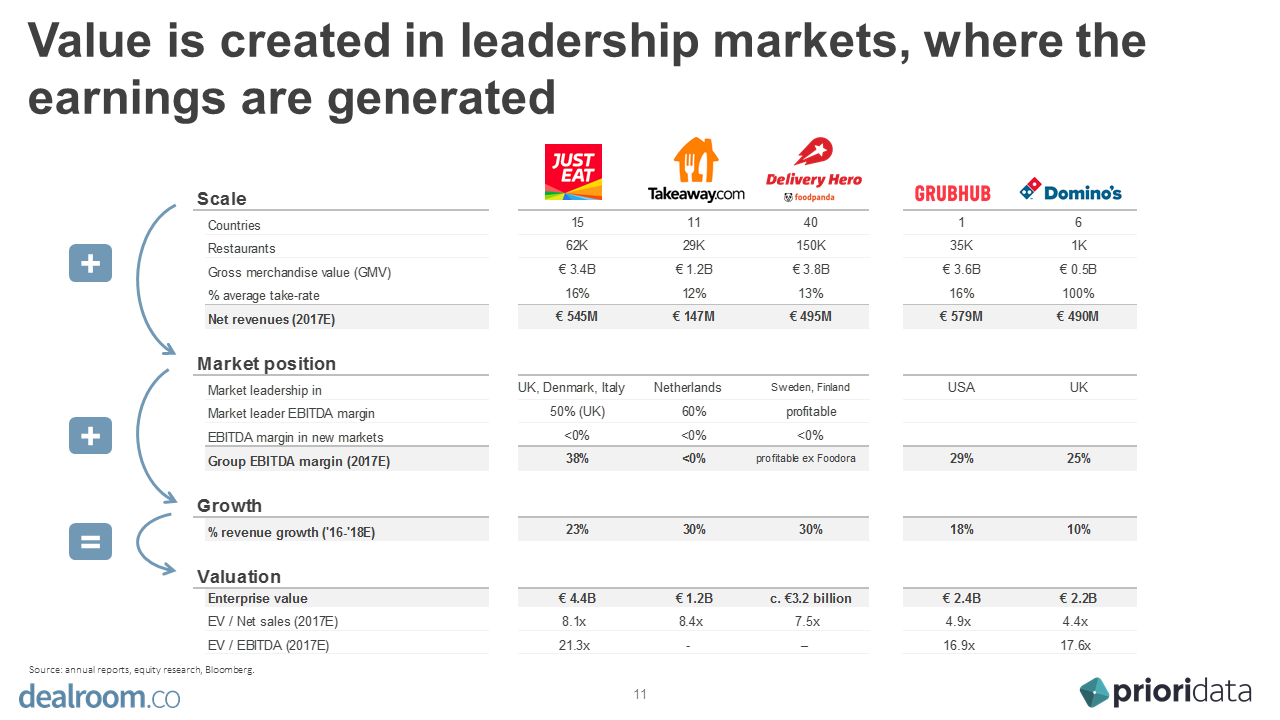

Dealroom recently did a deep-dive into the food tech space. The below table compares Delivery Hero’s numbers with it’s peers:

Naspers is obviously a highly experienced investor, but what should we make of this investment?

Delivery Hero’s strengths:

- Highest growth (excluding Deliveroo most likely)

- 2016 revenue growth: Delivery Hero 71%, Just Eat 52%, Takweaway 45%

- 2017 revenue growth estimate(1): Delivery Hero 40%, Just Eat 25%, Takweaway 30%

- Largest food network in the world with #1 positions in 35 of its 42 countries, most notably Turkey, South Korea, Germany (closely tied with Takeaway), Sweden, Finland, Greece and the Middle East. Delivery Hero covers an addressable market that is 3x larger than Just Eat and 6x larger than Takeaway

- Delivery Hero’s exposure to emerging markets has long-term growth appeal

- Arguably, not being public yet has given the company flexibility to operate a more aggressive growth strategy

Delivery Hero’s weaknesses:

- Unprofitable: Delivery Hero is on a path to profitability and management said it would be already profitable excluding Foodora. But while all food delivery players have profitable and unprofitable markets, at Delivery Hero the balance is tilted more towards loss-making positions, whereas Just Eat and Takeaway enjoy several major cash-cow positions

- Did not win in some head-to head situations

- Against Just Eat in the UK, Spain, Italy

- Against Takeaway in Poland (albeit still an early stage market) and Germany (where the two competitors are head-to-head)

- Most complex organisation (the flip-side of being in 40 countries, and now an integration with Food Panda)

- Low capital efficiency: $1.6 billion raised with a $3.5 billion valuation compares badly to both Just Eat (only $66M raised with a nearly $4.8B valuation), Takeaway ($90M raised with a $1.4B valuation)

Conclusion

Delivery Hero’s management has chosen a more risky strategy than it’s peers: expanding rapidly across the globe and investing more aggressively into its own fleet and logistics (via Foodora) than Just Eat and Takeaway.com did. Delivery Hero has been an easy target of cynicism due to it’s low capital efficiency and unprofitability. And for a moment it seemed like Delivery Hero was in a tough spot strategically. However, its 2016 revenue growth was ahead of expectations (71% versus 60% expected by analysts). This funding round from Naspers investments indicated strong Q1 2017 performance too. It now seems entirely possible that within a year or two, Delivery Hero’s vast scale, emerging markets and investments will start paying big dividends.

- Source: equity research.