Foodtech

Sponsored by

Foodtech is one of the main VC investment segments attracting on track to attract $13B of funding in 2023, and startups in the sector now have a combined value of $1.4T.

Foodtech startups raised $3.4B globally in Q2 2023, going back to 2019 pre-pandemic levels. VC funding has remained stable in Q1-Q3 2023 signaling that a new stable level of financing after the decline from peak.

Zooming out tough, foodtech VC investment increased more than 5x within the last decade.

The share of total VC funding going to foodtech has declined slightly from its all time high in 2018.

Foodtech accounted for 10% of VC funding at its peak in 2018, before decreasing steadily, especially in 2022-2023. The downfall of food delivery and other segments accounted for most of this change, while the climate tech part shows strong resilience, as we will see in the segment analysis.

Venture Capital

Comparison with other industries

Foodtech was the 7th most funded industry in 2023 so far, with over $12B in VC funding. Foodtech has seen a stronger slowdown than most other sectors, with a 53% funding drop from last year.

Foodtech investment by stage

Below we break venture capital into three distinct stages:

- Startup stage ($0-15M rounds)

- Breakout stage ($15-100M rounds)

- Scaleup stage ($100M+ rounds).

This provides more consistent and timeless segmentation of the startup & venture capital landscape (more so than self-reported round labeling, which are applied inconsistently, especially between business cycles).

Early-stage (<$15M) showed much stronger resilience with Q1 and Q2 2023 in line with 2021-2022 levels. Q3 is showing signs of the slowdown now hitting early-stage.

Breakout stage funding ($15-100M) has also decreased strongly from nearly $5B at peak to $1.3B in Q3 2023 and down 54% annually.

Late-stage funding ($100M+) has seen the strongest reduction, dropping from ~$9B in some quarters of 2021 to $1.6B in Q3 2023. Down nearly 2/3 annually.

Foodtech Investment by geography

Leading countries

The US attracted by far the most funding for Foodtech startups, with over $4B in 2023, notably followed by the UK and Germany. The UK is the top European country by Foodtech funding.

China's funding for Foodtech has decreased strongly, while India, the UK and France have shown a strong resilience to the downturn in the last two years.

Leading global hubs

Three of the top five hubs by Foodtech funding in 2023 are US based, with the Bay area taking the first spot.

London notably claims the second spot for VC funding in Foodtech in 2023. The fastest-growing top hubs are Munich and Stockholm.

Top Investors

Top Global Investors

Top European Investors

Combined Enterprise Value

The combined value of Foodtech startups has grown 40x in the last decade to $1.2T in 2023. Most of this value is still in the private market.

Younger cohorts of startups have already created most of the value, showing that value creation is accelerating in foodtech (the 2015+ cohort already accounts for more combined value than any other cohort).

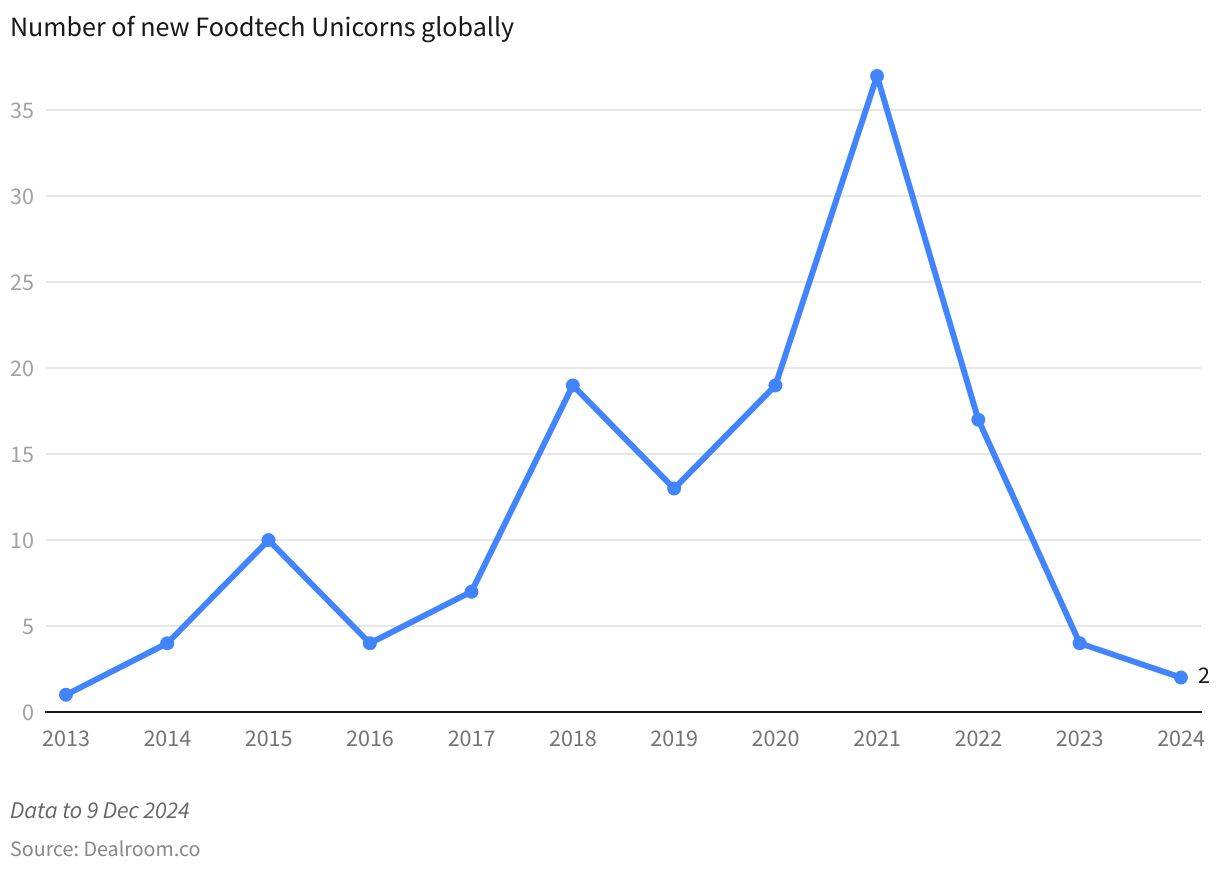

Unicorns

Unicorn creation has strongly dropped from a peak of 37 unicorns created in 2021 to just two in 2024.

Foodtech funding by segments

Foodtech funding has shifted massively in the years. Until 2021 most VC funding went to Food logistics & delivery, mostly driven by food delivery and groceries shopping. 2021 saw the rise and quick fall of 10-min delivery.

With the new market conditions, we see the rise of agritech in 2022 and 2023, which is more B2B oriented and resilient to consumer spending tightening. But even inside agritech, major shifts have taken place. Vertical farming has been one of the most invested segments in agritech but fell out of grace in 2023, while regenerative agriculture and carbon capture are quickly rising.

Alternative proteins were still nascent back in 2016, and peaked in 2021-2022, but are still one of the most funded segments in food tech. Major shifts have also happened in the different technologies and target markets. Discover more in the alternative protein section below

Explore the trends yourself by year and segment in the interactive graphic.

Food and Climate

The global food system is estimated to contribute 30% of total greenhouse gas emissions, with over half of those a result of livestock agriculture. Most of the impact is in the upstream phase. Agricultural production accounts for most of these emissions (such as methane emissions from livestock and rice and emissions from agriculture operations), followed by land use change (deforestation for animal grazing and feed production).

Downstream accounts for ~30% and comprises of emissions along the value chain (food processing, transport, packaging and retail) and post-retail (household food waste and cooking).

For these reasons, food has been increasingly incorporated into climate discussions, both in public and private spaces. Climate FoodTech startups started gaining momentum also in the VC space.

Climate tech now accounts for over one third of foodtech VC funding, up from just 11% in 2016.

Foodtech has though trailed behind other climate tech sectors attracting only 10% of climate tech VC funding in 2023, compared to a peak of 24% in 2020.

Food waste

Food waste accounts for approximately 6% of global GHG emissions (~3 Gigatons of CO2 equivalent per year). If food waste were a country, it would be the 3rd highest emitter after China and the US.

It is estimated that more than 1.3 billion tons of food (equal to approximately 13.8% of global food production) are wasted along the whole food supply chain.

Almost two-thirds of this (15% of food emissions) comes from losses in the supply chain, which result from poor storage and handling techniques, lack of refrigeration, and spoilage in transport and processing. The other 9% comes from food thrown away by retailers and consumers.

Three-quarters of food waste emissions come from meat and animal products, followed by nearly 29% for cereals and pulses.

According to Project Drawdown, food waste reduction is the #1 most effective solution under the scenario that limits end-of-century warming to 2°C.

Food waste VC funding peaked in 2021, attracting $1.6B. 2022-2023 funding is more or less back to 2020 levels at $500-700M in funding.

Food waste is a problem of one thousand cuts and needs a multitude of targeted solutions. Startups are tackling food waste from very different angles across the value chain and consumer stages.

A few key segments include:

- reducing waste in the supply chain: software for growers, distributors and retailers to avoid fresh food waste (onethird), food delivery to reduce food waste (Imperfect foods)

- extend food shelf life: using coating/packaging technology (Apeel Sciences)

- reducing food waste at restaurants and food distributors: extend food shelf life using coating/packaging technology (Apeel Sciences, Mori), dynamic labels (mimica), reusable containers (Pyxo), enables sales of unsold food items (Too good to go)

- better waste management: once the food is thrown away, it is still a hugely valuable resource to reuse, uplift or convert to energy. This depends on improving waste sorting, collection and management solutions. Examples include: waste management for businesses and municipalities (Recycle Track Systems), using organic waste as feed for insect farming (loopworm), transforming food waste into materials like bioplastics (UBQ Materials), and waste-to-energy (Impact bioenergy).

Discover 600+ food waste companies in Dealroom and explore food waste funding trends.

Alternative protein

According to a recent report by Boston Consulting Group (BCG), plant-based alternative proteins are by far the best climate investment.

For each dollar, investment in improving and scaling up the production of meat and dairy alternatives resulted in three times more greenhouse gas reductions than investment in green cement technology, seven times more than green buildings and 11 times more than zero-emission cars.

Farming for feed occupies 83% of the world's cropland, when including also feed production, with a huge impact on deforestation, impact on biodiversity loss and carbon emissions from

land-use change.

Lastly, the overconsumption of meat and other animal products, such as cheese, has a strong negative effect on people's health.

A recent Nature Food study found out that a dietary shift away from animal-sourced foods could save $7.3 trillion worth of production-related health burdens and ecosystem degradation while curbing carbon emissions.

There’s, therefore, the need to reduce consumption by at least 20% by 2030 in the West, and some studies point to a 90% reduction needed by 2050. However, instead of decreasing, demand for meat is expected to double by 2050.

Over $17B have been invested in alternative protein startups since 2016, with investments peaking at $5.6B in 2021.

Over 50% of the funding has been directed to plant-based alternative proteins, followed by precision fermentation and lab-grown (also called cultivated) proteins.

The share of funding going to plant-based alternative proteins has, however, declined from a peak of 66% in 2020 to 42% in 2023. Lab-grown instead peaked in 2022 at 28%.

Lab-grown

Lab-grown meat startups have raised over $2.7B since 2020, attracting nearly 20% of total funding in alternative proteins. The US is the leading country with over $1.5B in funding, followed by Israel, the UK and The Netherlands. There are now nearly 90 VC-backed startups worldwide.

There’s strong momentum around lab-grown meat, with the United States Department of Agriculture (USDA) approving in June 2023 the sale of lab-grown meat in the US, in particular, chicken products from UPSIDE Foods and GOOD Meat by Eat Just, Inc.

This makes the US the second country in the world, after Singapore, to allow the sale of meat grown from animal cells.

Israel’s Aleph Farms has also applied for regulatory approval to the Swiss Federal Food Safety and Veterinary Office (FSVO) to sell lab-grown meat in Switzerland.

This could make Switzerland the first European country to approve lab-grown meat. Italy is instead shaping to be the first country to ban it.

Explore 100+ lab-grown alternative protein startups.

Target food replacement

Most alternative protein startups focus on meat substitutes (Impossible Foods, Upside Foods, Aleph Farms, Mosameat). Followed by dairy, such as cheese and milk (PerfectDay, Oatly, TurtleTree, Vly).

But there are hundreds of other startups also offering alternatives to fish and seafood (Wildtype, BlueNalu, PrimeRoots); dairy such as cheese and milk (PerfectDay, Oatly, TurtleTree, Vly) and even products like eggs (Just, Perfeggt, Onego Bio) or chocolate (Planet A foods, Nu company).

Animal feed has received considerable funding, especially insects for livestock, aquaculture and pet food (InnovaFeed, Ynsect)

Discover 1.6K+ alternative protein startups in Dealroom and explore funding trends for alternative protein.

Pets food

The pet industry is one of the fastest-growing segments for foodtech startups to tap in, with an already huge market size of over $100B and growing more than 6% per year.

Pet food startups are on track to raise $1.1B in VC funding in 2023, more than twice than any other year before (compared with a general 53% drop for foodtech funding).

Startups are mostly innovating in the segment in two ways:

- Fresh and healthy pet food: startups such as Butternut Box and Lyka pet food offer subscription plans for pet owners to receive healthy fresh-cooked dog food.

- More sustainable pet food (alternative proteins): many startups are now offering pet food with alternative protein, either plant-based (Wild earth) or insect-based (Tomojo), which offers superior nutritional properties and health outcomes for the pets, while also having reduced emissions & environmental impact.

Discover 2.1K+ food x pet companies in Dealroom.

Partners

The first VC in Europe focused on innovative consumer-facing food companies.

Five Seasons Ventures back Food Tech entrepreneurs for a healthier, more sustainable and more efficient food system.

Five Season Ventures is the first VC fund in Europe solely focused on investing in innovative consumer food companies.

Related content

Reports: The State of European Foodtech 2023

Foodtech: Curated Content