Sponsored by

Though the % of total global VC is still quite small, bluetech has been steadily growing in importance.

In the last few years, most funding has gone into shipping and ports, such as freight forwarding and supply chain management solutions, especially in 2021-2022 after the pandemic supply chain disruptions.

Bluetech and ocean observation (mostly autonomous defense vessels), Shipping and ports and Shipbuilding and refit have instead dominated funding in 2025.

Though the % of total global VC is still quite small, bluetech has been steadily growing in importance.

In the last few years, most funding has gone into shipping and ports, such as freight forwarding and supply chain management solutions, especially in 2021-2022 after the pandemic supply chain disruptions.

Bluetech and ocean observation (mostly autonomous defense vessels), Shipping and ports and Shipbuilding and refit have instead dominated funding in 2025.

The Blue Economy ecosystem is still in an earlier stage of development with respect to more mature VC markets like fintech or even the broader climate tech space.

While the share of startups founded in the last five years is broadly comparable to climate tech, early-stage investment activity continues to significantly outpace exits, highlighting the sector’s relative immaturity.

The Blue Economy ecosystem is still in an earlier stage of development with respect to more mature VC markets like fintech or even the broader climate tech space.

While the share of startups founded in the last five years is broadly comparable to climate tech, early-stage investment activity continues to significantly outpace exits, highlighting the sector’s relative immaturity.

And our mapping of 260+ Algae and seaweed startups across 9 segments.

And our mapping of 260+ Algae and seaweed startups across 9 segments.

Key companies operating within this field on the abiotic side include Captura (using direct ocean capture, DOC, by extracting carbon absorbed by the ocean surface), Ebb Carbon and Heimdal (electrochemical ocean alkalinity enhancement by pumping out seawater and removing carbon), Limenet (using a carbon mineralization method able to transform the carbon dioxide collected from the atmosphere or other sources into an aqueous solution of calcium bicarbonates which helps ocean alkalinity).

On the biotic (nature-based solutions, NBS) side, most attention has been toward kelp and algae, with startups such as CarbonWave (large-scale Sargassum seaweed plantation to capture carbon and replace petrochemicals materials) and Brilliant Planet (which grows, dry and bury algae in the desert to remove carbon permanently).

Explore 100+ Ocean environmental protection and regeneration startups.

Leading accelerator and investor in impact startups and blue economy.

Leading accelerator and investor in impact startups and blue economy.

HUB AZUL Dealroom: a global ecosystem connecting blue innovators with investors

Forum Oceano: Portugal Blue Economy Cluster

HUB AZUL Dealroom: a global ecosystem connecting blue innovators with investors

Forum Oceano: Portugal Blue Economy Cluster

What is the Blue Economy?

The Blue Economy, or the ocean economy, is a term used to describe the economic activities associated with the oceans and seas. The World Bank defines the blue economy as the “sustainable use of ocean resources to benefit economies, livelihoods and ocean ecosystem health”, and the European Commission as “all economic activities related to oceans, seas, and coasts. It covers a wide range of interlinked established and emerging sectors”. The Blue Economy has existed for millennia and posed the base for developing a large part of our civilization. However, current economic trends have been rapidly degrading ocean resources. In response to this, a new generation of startups is now emerging to tackle the huge potential of the Blue Economy in terms of sustainable resource production and climate change mitigation for tremendous and regenerative blue growth. We break down the Blue Economy into 10 segments and over 30 subsegments. Explore the interactive chart by navigating the changes through the years. You can also click on a segment to zoom in and see the subsegments inside better.Why do oceans matter?

Covering two-thirds of the planet, the oceans play a vast role in the climate system. They have absorbed about 90% of the extra energy caused by global warming due to fossil fuels. As a result, the top 700 meters (2,300 feet) of the global ocean have warmed about 1.5°C since 1900. This, coupled with overfishing and pollution, is causing a rapid biodiversity decline in the ocean. In the latest assessment of global marine species, nearly 10% were found to be at risk of extinction, according to the International Union for Conservation of Nature (IUCN). Populations of marine vertebrates, specifically, (mammals, birds, fish and reptiles) declined by 49% since 1970, and 90% of stocks of large predatory fish, such as sharks, tuna, marlin, and swordfish, have already disappeared. The ocean also absorbs nearly one-quarter of all carbon emissions. However, due to all this carbon dioxide, it has become 26% more acidic since the 1940s (its pH has changed from 8.2 to 8.04 in 2020). Continuing on the same trend, pH in 2045 will drop to 7.95, a level at which it is estimated that 80% to 90% of all remaining marine life will be lost, triggering an irreversible tipping point for oceans. Economically, oceans represent a fundamental asset globally. The World Wide Fund for Nature (WWF) report conservatively valued the then-known “asset base” of the ocean at USD 24 trillion yearly, with USD 2.5 trillion in goods and services from coastal and oceanic environments – equivalent to the 7th largest economy by GDP in 2015. Over 80% of international trade is carried by sea, and the percentage is even higher for most developing countries. Furthermore, more than 3.5 billion people depend on the ocean for their food security, and approximately 350 million jobs are created in ocean-based sectors. When it comes to our climate transition, the ocean should be considered a key player both in adaptation and mitigation strategies against climate change. Oceans can help generate renewable energy through offshore wind and marine energy, helping to transition away from fossil fuels. Oceans are also important vehicles to remove and store carbon dioxide (CO2) from the atmosphere in natural systems. Finally, protecting and restoring ocean ecosystems, making fisheries and aquaculture climate-ready, and enhancing the resilience of coastal areas will all contribute directly to adapting to climate change's impacts on the ocean and communities.Blue Economy VC Trends

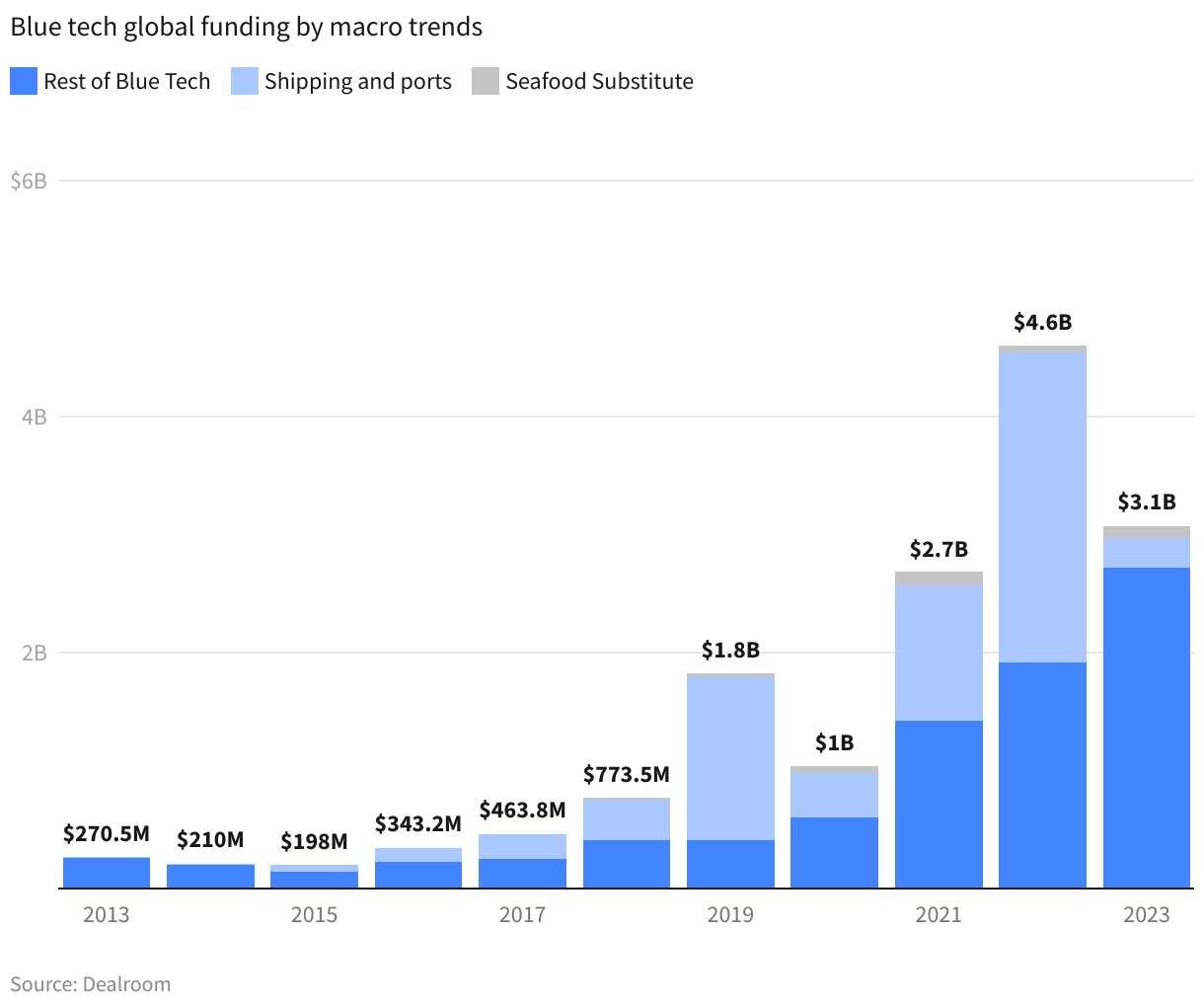

In recent years, there has been a major increase in awareness around oceans. The Blue Economy ecosystem has seen significant growth, reaching $3B in 2025. Blue economy VC funding has grown 5x in the last 8 years. When looking beyond shipping and ports, the rest of Blue Tech attracted $3B in 2025.VC allocation by stage

Below we break venture capital into three distinct stages:- Startup stage ($0-15M rounds)

- Breakout stage ($15-100M rounds)

- Scaleup ($100M+ rounds).

Comparison with other industries

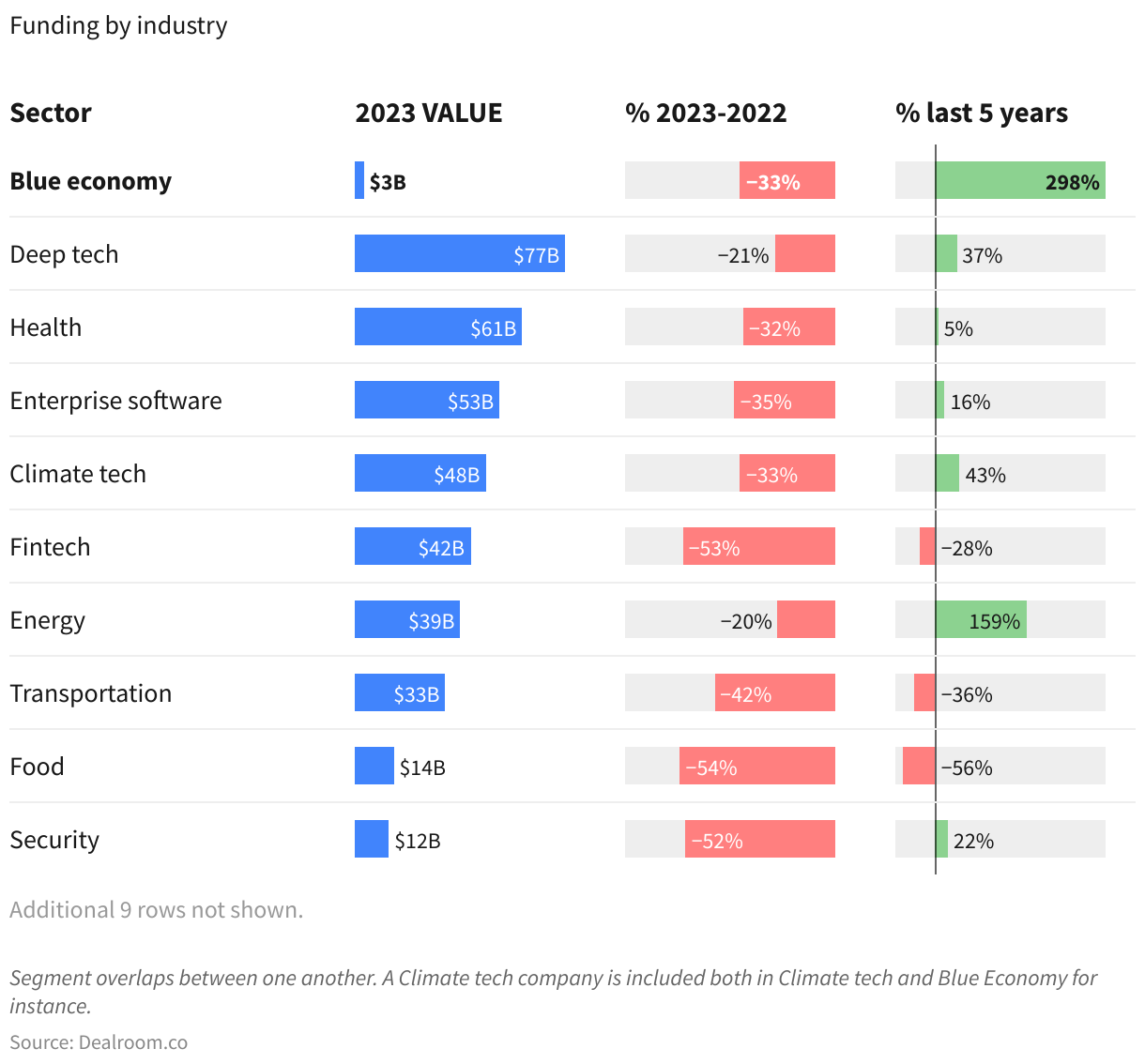

Blue Economy has been one of the fastest growing venture capital sectors, with a nearly 250% increase in the last five years, followed by Enterprise Software and Deep tech. It is still a much smaller overall market than many others, Climate tech attracted 8x more funding in 2024-2025. You can sort the table below by clicking on the columns.Top countries and regions

Iceland, Tunisia and Mozambique are the countries with the most share of funding going into the Blue Economy. Portugal and Norway also show a strong focus on the blue economy. The US regained momentum in bluetech VC funding in 2025, offsetting weaker investment activity in Europe and Asia. Despite regional divergence, funding remains concentrated in the US and Europe. The US is the leading country for 2025 blue economy investments, followed by the UK, Ireland and Iceland. Ireland experienced tremendous growth since 2024 following a no funding year in 2023.Oceans and Sea Basins

When analyzing the Blue Economy, we need to look beyond countries, regions, and continents to also Oceans and Sea Basins. Often, industry associations, partnerships and intercountry agreements are, in fact, shaped around these areas of operation. Considerable overlap exists among the different areas, with for instance US and Canada active in all Atlantic, Artic and Pacific regions, and Nordic countries such as Sweden and Norway active in both North Sea and Artic Sea. Since 2019, the Artic, Pacific and Atlantic, have attracted the most funding, mostly driven by the US. Looking beyond the US, The North Sea saw the strongest investments. You can explore each of the Oceans and Sea Basins on the Hub Azul platform.Blue Sectors

We break down the Blue Economy into 10 segments and over 30 subsegments. Explore the interactive chart by navigating the changes through the years. You can also click on a segment to zoom in and see the subsegments inside better.Shipping and ports

Shipping and ports is the segment that attracted the most funding from 2016 to 2025 in the Blue Economy with nearly $9B in VC funding. Over 80% of international trade is carried by sea, and the percentage is even higher for most developing countries. The Covid-19 pandemic showed how critical cargo shipping is and highlighted the need for better visibility, tracking and optimization of global shipping supply chains. VC funding in shipping and ports in fact peaked in 2022 at $2.7B in the afterwave of the pandemic, while 2023 saw less than $0.3B in funding. In shipping and ports, digital freight forwarding attracted the most investments, over $4.8B from 2016 to 2025, with platforms such as Flexport, Nowports and Xeneta helping companies to compare different logistics providers across price, timing and even emissions, as well as keep visibility and tracking of their shipping. These platforms usually integrate different logistics modalities such as ocean freight, air cargo and trucking. Supply chain tech also attracted vast funding, $2.5B from 2016-2025, with startups such as Project44 and Shippeo helping shippers optimize and maintain full visibility of their operations. Beyond freight forwarding and supply chain tech, some startups are focusing on reducing the GHG emissions from shipping thanks to emissions monitoring systems and carbon accounting (Green Sea Guard, Normative), operation control software (ZeroNorth, Nautilus Labs) Explore 150+ shipping and ports startups.Shipbuilding and refit

Global shipping accounts for 3% of worldwide greenhouse gases (GHG), and these emissions are projected to increase by up to 50% by 2050 from 2018 levels under a business-as-usual scenario. VC funding in Shipbuilding and refit startups has grown massively to nearly $0.7B in 2023, up 5x since 2020. The growth has been at all stages from early stage to megarounds. Over $2B have been invested from 2016-2025. Electrification has attracted nearly 50% of the investments in the segment, with a strong focus on ferries (Pascal technologies) and recreational boats (Pure watercraft), but also on batteries for long transport routes (Skoon Energy). Beyond electrification, many different approaches are being funded to decarbonize maritime shipping, such as hydrogen (Eodev, Hyon), ammonia (Amogy), other low-carbon fuels (Carbon One), auxiliary wind (Norsepower, Ayro), nuclear fission (CORE-POWER), waste heat recovery (Orcan Energy), point-source carbon capture (Seabound) and fouling, foils and other optimization (Hullbot, Wavefoil). Explore 130+ Shipbuilding and refit startups.Blue Renewable Energy

VC funding in Blue renewable energy startups has grown from less than $100M per year in 2018-2020 to more than $300M in 2022 and 2023. However, 2024 declined almost by half compared to these record highs. Over $1B have been invested since 2016. Offshore wind attracted nearly 3/4 of all Blue renewable energy funding. This is not surprising since offshore wind is the most mature of the ocean's renewable energy sources. In the US, it is estimated that offshore wind potential exists for over 4,000 GW of capacity —more than three times the country’s installed electricity generation capacity. Companies in the field include Venterra (offshore wind services), Gazelle Wind Power (hybrid floating offshore wind platforms), and Principle Power (wind turbine agnostic floating platform). Wave and tidal energy is still in the early stages of development despite having the potential to exceed the global power demand of 22,848 TWh/y. There are several methods of producing energy, and they commonly involve placing electricity generators on the ocean's surface, but also submarine installations. Ever since its uptake in 1973, several conversion technologies were introduced in the market, with different characteristics and deployment suitability. Companies operating within this field include AW-Energy and CorPower Ocean. Even more nascent is the segment of ocean thermal energy, which exploits thermal energy harvesting systems to create electricity underwater from temperature differences in the ocean. Early innovators include Seatrec and Global OTEC Resources. Floating solar panels are also gaining interest from investors, with a record $18M of funding in 2023, up from nearly nothing in 2018-2019, but the sector is still in a very early stage. Examples of companies include Solar Duck and Oceans of Energy. Some of the main advantages of floating solar are space utilization (no land use) and better efficiency, thanks to the cooling effect from water. However, they also suffer from typical offshore installation challenges such as high maintenance and infrastructure costs (foundation, grid connection, etc). Floating solar accounted for less than 1% of total solar installations in 2022 and accounted for only 0.003% of all solar energy VC funding in 2023. Overall, Blue renewable energy attracted less than 2% of global renewable energy VC funding in 2024. Marine energy can be a challenging resource to harness: salt water and sediment could damage ocean-bound machines; devices must be able to withstand strong wave and tidal conditions; and deploying or servicing devices offshore can be costly in terms of time and money. Hence, higher costs, natural barriers and lower technology readiness play an important role in the development of this market. Explore our mapping of 130+ Blue renewable energy startups across 4 categories.

Bluetech and ocean observation

VC funding in Bluetech and ocean observation has already reached a record high of $1.9B in 2026YTD, a 250% increase from 2024 and 920% increase from 2023 due to megarounds. Over $3.5B have been invested from 2016-2025. Drones, surface and subsea robots have attracted 70% of the funding in the sector. Example of companies include Saildrone (operating fleets of autonomous surface drones for defense and ocean mapping), Bedrock Ocean Exploration (autonomous vehicles for seafloor mapping), Skyspects (drones for offshore wind turbines inspection and maintenance), and Tekever (drones for monitoring of ocean activities). Space tech for maritime monitoring is also attracting considerable funding, such as Unseenlabs, which enables the tracking of maritime vessels at any location using satellite data. Another interesting segment is underwater communication, such as Wsense. Explore 380+ Bluetech and ocean observation startups.Blue biotechnology

Blue biotechnologies, or marine biotechnologies, are processes that transform marine resources into services and goods in a multitude of fields. These include microorganisms (microalgae, bacteria, and fungi), seaweed & algae, and invertebrates (e.g., starfish, sea cucumbers, and sea urchins). VC funding in Bluetech biotechnology peaked at over $900M in 2022 and dropped to ~$400M in 2023.. Over $3B have been invested since 2016. Half of the funding into this segment went into seaweed and algae startups for a variety of applications. Applications range from pharma (Lumen Bioscience uses a patented technology to use the well-known food algae spirulina to deliver therapeutic proteins), food (Brevel develops microalgae-based alternative proteins), feed supplements for cow methane emission reduction (CH4 global) and biomaterials & biofuels (Viridos produces sustainable, low-carbon, algae-based jet and diesel fuel; Sway seaweed-based bioplastic). Beyond seaweed and algae, some startups are exploiting other marine resources for innovative applications, such as Jellagen, which uses jellyfish to produce Collagen Type 0 for complex tissue engineering and regenerative medical needs, and Hemarina which develops marine oxygen carriers for industrial and therapeutic applications based on the particularities of purified hemoglobin from lugworms, Arenicola marina. Explore our mapping of 300+ Blue biotechnology startups categorized across 7 segments.

And our mapping of 260+ Algae and seaweed startups across 9 segments.

Ocean environmental protection and regeneration

VC funding in Ocean environmental protection and regeneration has increased strongly in the last three years, with the first companies in the segment starting to raise Series B+ rounds. 2024 was a record high year with over $200M raised, representing a quarter of the $900M that have been invested since 2016. The ocean is one of the main repositories of the world's biodiversity, counting over 90% of the habitable space on the planet and contains some 250,000 known species. Such biodiversity is crucial for innumerable life aspects, from social to economic and environmental. Yet, just 3.4% of the ocean is protected, and only part of this is effectively managed. As a consequence, nearly 10% of marine species are found to be at risk of extinction, with climate change impacting at least 41% of threatened marine species. Populations of marine vertebrates, specifically, (mammals, birds, fish and reptiles) declined by 49% since 1970. Over $200M since 2016 has been invested into ocean biodiversity protection and tracking, across biodiversity tracking startups such as Spoor (SaaS data platform that enables continuous monitoring of wildlife for offshore wind farms, pre and post construction), and biodiversity regeneration startups such as Urchinomics (which removes overgrazing sea urchins which helps turn a barren seafloor back into a vibrant kelp forest), and Coral Vita (using proprietary technology to grow resilient corals 50x faster to restore dying reefs.). Ocean carbon removal (CDR) is also starting to pick up, with $82M raised in 2024. This accounted for 10% of overall carbon removal, which has so far mostly focused on land, a still low share but the highest historically. Oceans are in fact naturally key carbon sinks, absorbing nearly one-quarter of all carbon emissions. This has, however, caused the ocean to become 26% more acidic since the 1940s (its pH has changed from 8.2 to 8.04 in 2020) and might see a drop to 7.95 by 2045, a level at which it is estimated that 80% to 90% of all remaining marine life will be lost, triggering an irreversible tipping point for oceans. Ocean CDR aims, therefore, to leverage the ocean’s natural chemical and biological processes to capture and remove carbon from the atmosphere while often also reducing the adicity (enhancing the alkalinity) of the ocean. Ocean CDR spans a wide range of approaches, each with different levels of scientific reliability and efficacy. Overall, seven main approaches are thought to be the most effective and scalable from biotic approaches such as coastal wetland & mangroves restoration and seaweed (especially kelp) cultivation, to engineered approaches like alkalinity enhancements and electrochemical CO2 removal.

Fisheries

The fisheries startup sector is very nascent, having attracted just over $530M since 2016. Funding has picked up at $150M in 2022, before a decline in 2025. Still, 2025 has still seen more investments than any year beyond 2021-2022. Most funding has gone into seafood logistics & marketplaces such as Captain Fresh (a B2B marketplace for seafood integrating and tracking all steps of the value chain from procurement to retail) and Seafood Souq (offering a transparent and traced marketplace for seafood trade and blue financing solutions to empower sustainable fishing practices in emerging markets). Startups improving the sustainability of fishing techniques themselves are also attracting funding, such as Ava Ocean (reinvent seabed harvesting from a destructive practice to one enabling revitalization and preservation of vital marine ecosystems) and Blue Ocean Gear (prevents the economic and ecological impact, one of the largest sources of plastic waste in the ocean, of lost gear through IoT tracking technology). Fish compose a small amount of global protein intake (6.7%) and 17% of animal proteins. More than 3.3 billion people around the world depend on fish for at least 20% of their animal protein intake, and in many developing countries, seafood accounts for more than 50% of the total animal protein intake. Globally, 58.5 million people are employed in the fishing industry or related jobs. But overfishing has left some fish stocks depleted, while destructive fishing practices like dredging have harmed ecosystems. Explore 20+ fisheries startups on the platform.Aquaculture

VC funding in aquaculture startups has reached a record level in 2022 with $750M, growing 2.6x since 2021. 2024 fell 2 fold short of that with $270M in funding, nearing pre 2022-2023 peak levels. Overall, over $2B have been invested in aquaculture startups since 2016. With rising demand, oceans have been subject to overexploitation and an important strain on biodiversity and marine resources. Overshing, specifically, has led both freshwater and ocean fish populations to plummet to unsustainable levels. Worldwide, due to overfishing, 90% of stocks of large predatory fish, such as sharks, tuna, marlin, and swordfish, have already disappeared, and many other smaller species stocks are decreasing. To cope with this, aquaculture has been increasingly the answer in the last three decades. Fish farming, in particular, has enabled seafood consumption to continue to increase even as marine fisheries production has flat-lined. It now supplies 58% of the fish we eat, has kept the overall price of fish down, and has made protein and improved nutrition more accessible to communities around the world. Yet, not all aquaculture practices are sustainable. In many countries, aquaculture production continues to deplete ecosystems and threaten the ocean’s health. Seaweed and mussel farms have been to improve biodiversity and abundance of marine life, while salmon farming has had catastrophic effects on wild fish stocks due to escapes, heavy use of antibiotics, and the need for fish feed. Among the main sustainable aquaculture solutions, we have deep ocean aquaculture of bivalves (Oceano Fresco), antibiotic and vaccine-free renewable energy-powered aquaculture (The Kingfish Company), and controlled land aquaculture with zero antibiotics (LISAqua). Explore 130+ aquaculture startups on the platform. Finally, alternative protein fish substitute products, which are not included in the statistics above, have also attracted over $700M since 2016. Most attention has gone into lab-grown seafood alternatives such as Wildtype and Bluenalu (lab-grown sushi-grade salmon), and Blue Seafood (lab-grown fish products starting from fish sticks and fish balls).Coastal and marine tourism

Coastal and marine tourism has seen marginal VC and startup activity, with less than $215M since 2016. . Examples of startups in the sector include Brim Explorer (which provides ocean excursions without noise or pollution on board silent electric and hybrid-electric passenger ships) and Dockwa (app that provides reservations to boaters and the marine industry). Explore 10+ Coastal and marine startups.Water management

VC funding into water management startups in 2023 has been more than double that of any previous year, showing impressive growth. Overall, 2024 funding reached $330M, a 60% decline compared to the previous year's record highs. Overall, over $2.2B has been invested since 2016. Wastewater treatment (the treatment of water coming from industrial processes, agriculture or residential use before discharge) has attracted the vast majority of investments. While not strictly an activity carried out in the ocean, it has a huge impact, causing the pollutants, chemicals, organic waste, and plastic reversed into rivers to end up in the ocean, destroying sealife and causing algae blooms. Examples of companies include Gradiant (an end-to-end solutions provider of advanced water and wastewater treatment for large industrial corporates), Solugen (bio-based chemicals for water treatment) and Puraffinity (which develops precision technology for the removal of PFAS "forever chemicals" across water treatment applications). Other water management startups focus on water monitoring and treatment beyond wastewater, such as BlueGreen Water Technologies (which offers a technology suite to reverse the effects of climate change on lakes and oceans, starting with a focus on harmful algal blooms). Desalination is another key area which is attracting investors' attention due to increasing water scarcity. It is predicted that over half of the population will live in areas subject to water scarcity for at least one month each year. Desalination can help alleviate water stress and diversify water supply for more resilience. Desalination is usually coupled with renewable energy sources such as wave energy like Ocean Oasis (zero emission offshore desalination solution) or solar energy like Boreal Light (affordable solar water desalination systems for off-grid communities). Plastic pollution is another major focus area for water management. At least 14 million tons of plastic end up in the ocean every year, and plastic makes up 80% of all marine debris found from surface waters to deep-sea sediments. In the last few years, an ecosystem of startups tackling marine plastic pollution emerged. Startups in this ecosystem are dedicated to either picking up, recycling, reusing, and recovering plastic from the ocean. Examples include The Ocean Cleanup, Matter and Cleanhub. The manufacturing of ocean-based plastic alternatives is instead discussed in blue biotechnology. Explore 275+ water management startups.Top investors, accelerators and ecosystem actors

Top Investors

Blue economy specialists and climate tech VCs make up the most active investors in the sector. Notable is also the strong activity of SOSV, a generalist fund with a strong climate activity focus.Top Accelerators

Blue economy specialists and climate tech accelerators are the most active early supporters of blue economy startups.Ports

Ports play a crucial role in the blue economy as they are essential gateways connecting land and sea, facilitating international trade and commerce. However, their significance extends beyond conventional maritime activities. Ports can potentially become dynamic hubs for startups that are driving innovation in the ocean sector. Ports possess critical infrastructure, logistical capabilities, and established networks, making them ideal locations for startups to establish their operations. By leveraging the resources and expertise available at ports, startups can capitalize on the blue economy's vast opportunities and develop innovative solutions to address various challenges. Collaborations between ports and startups can lead to novel solutions in sustainable aquaculture, renewable energy, marine robotics, and beyond, driving economic growth, fostering job creation, and contributing to the sustainable development of the oceans. In summary, ports are fundamental actors in the blue economy due to their strategic location and existing infrastructure. They have the potential to become innovation hubs, attracting startups that aim to revolutionize various sectors within the ocean economy.Structural Challenges

The blue economy startup ecosystem is overall still in its early days. This is not only due to a lack of awareness of the topic but also to some structural challenges tied to the scaling of the blue economy. A significant challenge lies in obtaining consistent and quantifiable data. Without reliable scientific data, fostering a market with investable ocean projects and innovations is problematic. Due to the shifting nature of the open ocean and deep seas, gathering data at great depths and pressures is both a logistical and scientific challenge. Overall, ocean-related scientific study is estimated to account for only between 0.04% and 4% of total R&D expenditure worldwide. As of today, the deep ocean is considered to be the least-known environment on Earth, with approximately 90% of the species that researchers collect in the abyssal zones being new to science. Besides data gaps, the absence of clear governance arrangements in areas beyond national Exclusive Economic Zones (EEZs) also makes it difficult to implement projects and attribute responsibility for impact to specific agencies and countries. Indeed, on land, offset projects are normally implemented within areas with defined ecological and political boundaries, and clear agents. Oceans, instead, are characterized by undefined geopolitical boundaries, a lack of precise agencies to oversee projects and mandate responsibilities.Public Blue Economy initiatives

Despite such challenges, the last years have seen important improvements and initiatives rising both in the public and private realms. We have summarized below a list of the main institutional and public initiatives created in recent years that are inevitably connected with the unfolding of private ocean-tech innovations. The ‘BlueInvest’ investment platform was launched by the European Commission in April 2019, with the goal of fostering investment, innovation and sustainable growth in the Blue Economy. The platform supports innovative SMEs and start-ups active in the Blue Economy sectors, through its online community, investment readiness assistance, matchmaking, investor outreach and engagement, its academy, projects pipeline and a BlueInvest Fund. The 1000 Ocean Startups coalition was launched in 2021 and unites the global ecosystem of incubators, accelerators, competitions and investors supporting startups for ocean impact. The Convention on Biological Diversity’s (CBD) Fifteenth Conference of the Parties (COP 15), which took place in Montreal from December 7 to 19, 2022. Here, countries pledged to protect 30% of the ocean, land and coastal areas by 2030 (known as ‘30×30’). This was a first important step to bridging the blue economy and climate regimes, enabling the UN 2030 Agenda for Sustainable Development. In 2023, member states of the United Nations agreed to a High Seas Treaty that ensures the protection and sustainable use of marine biodiversity in areas beyond national jurisdiction. For the first time in history, rules will be in place to effectively manage and govern oceans. The High Seas Treaty includes an agreement to impose strict ocean protection outside national borders and rules for the sustainable use of its resources. Ocean Climate Action Plan in the USA. The OCAP is a policy framework introduced in 2023 under the Biden-Harris Administration to safeguard oceans and coastal communities. The Ocean Climate Action Plan entails deploying offshore energy infrastructure (wind & marine energy); investing in marine conservation through nature-based solutions and carbon removal; and decarbonising marine shipping and transportation.Blue Economy Clusters

Blue Clusters are key strategic organisations for accelerating sustainable and competitive innovation in the ocean economy. Blue Clusters are the honest brokers of the ecosystem since, in each country, they aggregate all relevant actors - startups, corporates, universities, R&D Centres, Investment Funds, Banks, and Municipalities - towards shared action in structural projects that are useful for deploying new technologies and testing new products and services.Partners

Leading accelerator and investor in impact startups and blue economy.

Katapult VC is a global investment company focusing on early-stage impact-driven technology startups. Katapult has, over the last 5 years, made 178 investments in impact tech startups from 47 different countries. Katapult invests within three investment verticals: Ocean, Climate and Food-tech.

Katapult has run nine flagship accelerator programs and three corporate accelerator programs.

In 2021, Katapult also launched the Katapult Foundation with the aim of building a larger network around impact investing. Katapult also hosts the annual Katapult Future Fest in Oslo, bringing together founders, investors and some of the most prominent figures within the impact investment sector.

HUB AZUL Dealroom: a global ecosystem connecting blue innovators with investors

Hub Azul Dealroom is the digital platform for the global internationalization of Portugal's Blue Economy, ignited by Fórum Oceano (Portugal's Blue Economy Cluster), in articulation with the Strategic Management Council presided by the Directorate General for Maritime Policy of the Ministry of Economy and Sea of Portugal.

Hub Azul Dealroom is financed by the Next Generation EU Fund - Recovery and Resilience Plan of Portugal.

Fórum Oceano is the entity that manages the Portuguese Sea Cluster.

Fórum Oceano's mission is to reinforce strategic cooperation dynamics between actors – companies, RTD centres, higher education institutions, Public Administration bodies – to promote innovation, qualified employment and the competitiveness of companies that use the Sea and marine resources as central elements of their activity.

As part of its mission, Fórum Oceano intends to contribute to the digitization, decarbonisation and circularity of the Sea Economy’s production processes.

Related Content

Impact Methodology & Definitions: Learn how Dealroom defines impact here. Platform: Explore our Blue Economy platform.